The “New Normal” for Motor Dealers

The operationalizing of motor dealers and motor manufacturers in SA under level 4 and 3 lockdown regulations, will not be business as normal. The new term being used across the world is the “new normal”.

The new normal means doing business considering the risks of the Covid19 pandemic on the market and customers (demand), provision of material and parts for manufacturing (supply), availability of motor vehicle stock and the safety of dealer staff (supply), changes in consumer buying patterns (consumer behaviour) and the connectivity between these critical components of the motor industry (accessibility).

With the outbreak of the pandemic in China, the immediate impact was the falling away of the supply side. Once this had hit rock bottom across the globe, there was a concomitant dropping away of demand. The global motor industry has had severe supply chain interruptions, the closure of manufacturing plants, unsold vehicles and inventories sky-rocketing and new vehicle sales plummeting. The shutdown of the global motor industry for two months was projected to see a 7-11% loss in the global economy.

Both worldwide and in South Africa, the motor industry is starting to open factories and dealers are gearing up to assist customers with car sales, servicing and spare parts as lockdown regulations are eased. There is no doubt that it will take some time for the supply side to get back to the “new normal”. This will require all suppliers to the motor industry becoming operational and supply chains functioning at full capacity.

For the motor industry to become operational will require government entities and the private sector to become fully functional as well. For example, financial institutions responsible for the issuing of loans to purchase cars will need to come to the party and ensure quick and effective transfer of funds. The departments responsible for licensing new vehicles will need to open up and do their jobs understanding the “new normal” within which the motor industry is operating. The “new normal” may be an invaluable opportunity for the inclusion of innovative technologies to facilitate improved processes in financing and licencing of motor vehicles.

There are many uncertainties remaining in the motor industry of which one of the most critical is on the demand side and that is whether customers will be wanting or able to buy new cars in the foreseeable future.

Changing Market Dynamics of Motor Dealers

Where the average customer in South Africa replaces a vehicle after just more than three years, it is likely that they will now keep their vehicle for longer. With the high level of uncertainty in job retention, people will be holding onto whatever financial reserves they have to sustain their livelihoods and pay for other emergency expenses. Consequently, demand in coming months will be dampened and with motor vehicles sales being a lead indicator, this does not bode well for the South African economy as a whole.

New car sales have declined by 13.8% month-on-month and 29.7% year-on-year in April. This after a decline of 15.9% month-on-month and 13.5% year-on-year in March. TransUnion figures show a year-on-year decline of 35% in financing new vehicle purchases in March and 31% for used vehicles. Passenger vehicle sales were down by 17% in March while commercial vehicles sales were down by 13.6%.

People are being more cautious and if they have budgeted, or need to replace their car, they are choosing to buy second-hand vehicles. This is reflected in the marginal year on year increase in the pre-owned motor vehicle market and TransUnion’s Vehicle Price Index (VPI) showing that just over two second-hand vehicles are being sold to each new vehicle. A Nedbank report warned that the situation in the motor industry would get worse and it has.

Opportunities at the end of the Covid19 tunnel

The continued revising of the repo rate to 4.25% will make it more attractive for customers to buy new and used vehicles. This is possibly over a longer repayment period, with no deposit and with larger residuals to counter for potential vulnerabilities that may arise as the pandemic matures in South Africa and elsewhere. Although allowing consumers more options to buy vehicles, it will place further pressure on dealers who are already feeling the financial strain from a stagnant economy and the lockdown.

The motor industry will have to further incentivize the buying of vehicles as it has done so effectively in the past. Original Equipment Manufacturers (OEM) and dealers will need to review their vehicle pricing, which increased by 4% year-on-year in the first quarter of 2020. Other dealer incentives, such as cash back or better maintenance schemes may well encourage customers to make the leap and buy new or used vehicles. Consumers will also look more carefully at the make, vehicle type (eg sedan, SUV, light commercial) and price range. TransUnion figures show that purchasing of vehicles in the price range below R300 000 has seen more consistent growth while vehicles in the higher price ranges have declined. This reflecting the stagnant economic growth in the country over recent years.

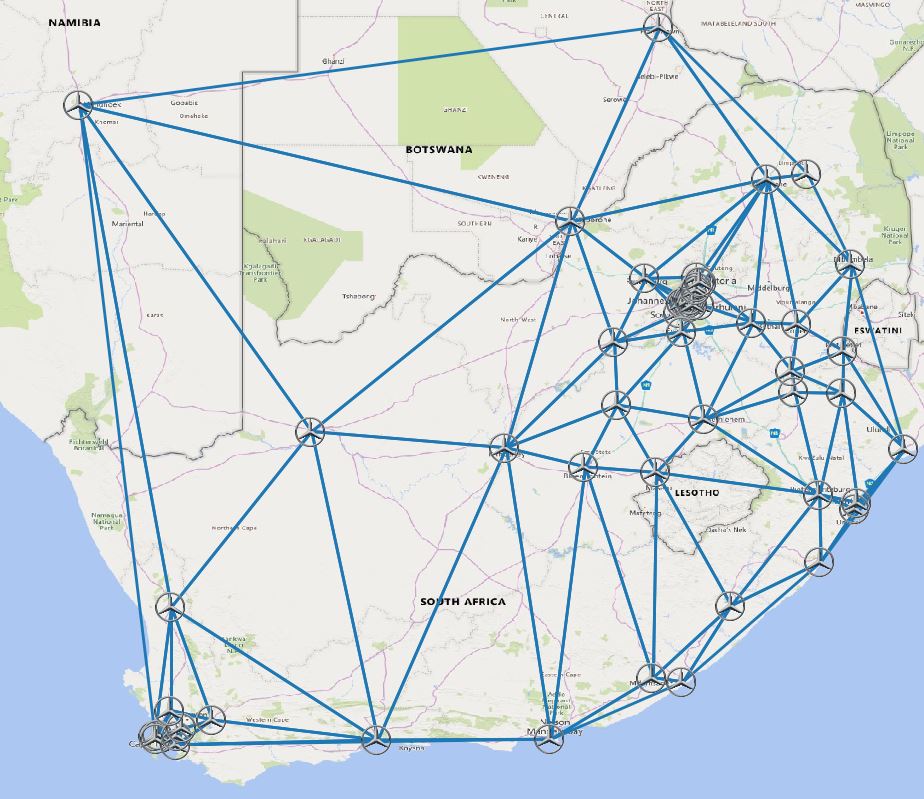

Mapping Dealer Trade Areas a First Step

,

A key part of the “new normal” in the motor industry will be the ability of OEM’s, dealers groups and independent dealers to access accurate and reliable information so that they can understand how their market is changing. A critical first step is to map the location of all dealers so that their trade areas can be defined. The originator of the trade area concept was Huff in 1963, who described it as the area from which a majority of a dealer’s sales and service clients originate from. The best way to define the primary and secondary trade areas of a dealer is to access customer databases and to map their location.

The primary trade is where 60% of the closest customers come from and the secondary trade area is where 80% of customers come from. The primary trade has been shown to be the minimum area required for a dealer to be financially viable while the secondary trade area is the market that enables a dealer to be profitable. A key advantage of defining the trade area is that it enables the average travel time of customers reaching dealers of different sizes to be calculated.

In instances where motor companies do not have a database of their customers (which would be unusual), an alternative approach is to define the target market of the dealer’s brands and to calculate the minimum number of customers that are needed to enable them to be financially viable.

When it comes to passenger vehicles, it is normally the current individual and household income data that is used to define the target market. A factor that is often overlooked when defining the target market, is the inclusion of the daytime or working population with its own unique income characteristics. When focusing on commercial vehicles, the data on Gross Geographic Product (GGP) is used to define the size of the market.

Using transport network based accessibility models the trade area for dealers can be defined. These trade areas can then be used as the Dealers Marketing Area (DMA). By law it is required that the DMA allocated by the OEM to the franchised dealer is large enough to provide access to a target market of the right socio-economic character, so that they can be financially viable.

Once the trade area has been defined, other geospatial information can be provided for that dealer. This can include consumer data, such as that from the Media and Product Survey (MAPS) and its geocoded component, which will be available from the Market Research Foundation (MRF) in coming months. Information on the population size by age and gender, income, GGP, the location of competitor dealers and other retail sites as well as shopping malls can be provided for the trade area. Having defined the trade area or DMA, information on media channels available to the dealer can be integrated to provide a much more targeted marketing strategy.

Research for large OEM’s in the past has shown that when comparing the trade areas using their customer base to that define using the size of the target market, dealers in most instances are following a shotgun approach with their marketing. Meaning that they are reaching far beyond their DMA in making sales to customers, which results in them cannibalizing neighbouring dealer territories. In some instances, this is a reflection that the DMA defined without the use of network based accessibility studies, does not have enough market of the right socio-economic character for it to be sustainable. Dealers in the “new normal” will need to have targeted marketing strategies to maximize their sales within their DMA.

Sales Target Setting & Dealer Network Optimization

,

With the integration of sales volumes from the dealer into the trade area with data on the size of the target market, annual sales target setting can be done for all dealers in the network. Having done this for several OEM’s in South Africa, it has shown that it is a method that is often more accepted by dealer principles than the methods presently being used by OEM’s. Not only is it more scientific and transparent but it ensures that changes in the characteristics of the market in the DMA is considered annually before setting sales targets.

South Africa is fortunate that many of the OEM have used network based accessibility studies to define the number and optimum location of dealers in their network. So, their dealers are optimally located in their networks and many will be able to withstand the ruptures in the market.

Most of the OEM’s have implemented expansion strategies in the past to grow their networks. Others have rationalized their dealers to get to an optimum network size. This is so that they could stabilize their brand and look for future growth, having improved their vehicle range, pricing & marketing strategies.

Those OEM’s that have used simple univariate feasibility or gap analysis may find that many of their dealers in their network are not optimally located and in this more stressed economic environment, may need to close.

Kriben Reddy, TransUnion’s vice president of auto information solutions has been quoted as saying “this is a tough time for car dealers, who must use this opportunity to make changes to remain competitive in a post-pandemic world”. He is absolutely right and to maximize the opportunity and their competitiveness, the use of relevant information and innovative approaches is required. He was also been quoted as saying “the lockdown will impact the way that consumers and dealers do business in the future.”

It is not business as usual, it is all about the “new normal” and that requires OEMs, dealer groups and independent dealers to use information and appropriate network based accessibility studies to optimize their dealer networks and provide realistic sales targets so that they can stabilize their market and look for growth in the future.

Bibliography

,

BusinessTech. 2020. Here’s how the car market will change in South Africa after lockdown is lifted. 25 April 2020.

,Leggett, T. 2020. Coronavirus: How can the car industry hope to recover? BBC News. 2020. 14 May 2020.

Nedbank Group Economic Unit. 2020. Nedbank – guide to the economy. February 2020.

West, E. 2020. Motor dealer industry stalled in SA, thousands of jobs on the line. IOL. 5 May 2020.

About the Author

,Craig Schwabe, is a geospatial specialist and focuses on the development of geospatial data for South Africa and Africa. He also specializes in the use of accessibility modelling in the provision of government services and optimizing the location of private sector outlets.

Craig has assisted some of the largest motor manufacturers and second hand motor dealer groups in South Africa with optimizing their dealer networks, defining dealer trade areas and setting sales targets including Auto Pedigree, BMW, Fiat, Iveco, Mazda, Mercedes-Benz, Mini, ,Nissan, Suzuki and Volvo. ,Craig has published several reports, books, chapters and scientific papers as well as presented papers at a number of national and international conferences.

,Download document

,While every effort has been taken to ensure the accuracy of the information and views contained in this document, no responsibility can be assumed

,for any actions taken based thereon,.